- Market Overview

- Futures

- Options

- Custom Charts

- Spread Charts

- Market Heat Maps

- Historical Data

- Stocks

- Real-Time Markets

- Site Register

- Mobile Website

- Trading Calendar

- Futures 101

- Commodity Symbols

- Real-Time Quotes

- CME Resource Center

- Farmer's Almanac

- USDA Reports

Host Hotels & Resorts Stock: Is HST Underperforming the Real Estate Sector?

Host Hotels & Resorts, Inc. (HST) is a leading real estate investment trust (REIT) that primarily focuses on owning and managing luxury and upscale hotels in top markets across the United States and internationally. The company is headquartered in Bethesda, Maryland and its portfolio includes a wide range of hotel properties, including those under renowned brands like Marriott, Hyatt, and Hilton.

Companies with a market capitalization between $2 billion and $10 billion are generally classified as 'mid-cap stocks,' and HST, with a market cap of nearly $10 billion, fits squarely within this category. Known for its strategic focus on prime locations and high-quality properties, HST is well-positioned to benefit from the growing demand for luxury accommodations. Its strong dividend payouts also make it an appealing choice for income-driven investors.

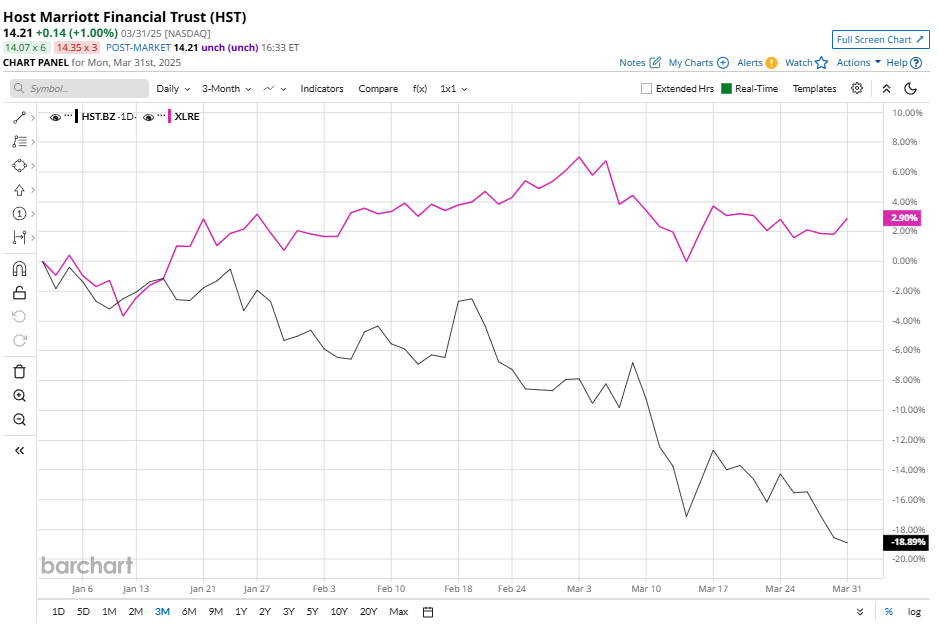

Despite these advantages, HST has faced significant challenges recently. It has retreated 31.9% from its 52-week high of $20.85, reached on April 1 last year. Shares of the REIT have declined 21% over the past three months, compared to the Real Estate Select Sector SPDR Fund’s (XLRE) 3.2% rise during the same time frame.

Zooming out, HST has declined 31.3% over the past 52 weeks, sharply trailing XLRE’s 5.9% gain. Even over the last six months, HST has fallen 21.6%, while XLRE only dipped 5.5%.

Furthermore, HST has been trading below both its 50-day and 200-day moving averages since late December, signaling a downtrend in the stock.

Host Hotels & Resorts shares slipped over 1% on Mar. 10 following a downgrade by Compass Point Research & Trading LLC, which lowered its rating on the stock from "Buy" to "Neutral."

Despite facing challenges of its own, HST has outpaced its rival, Pebblebrook Hotel Trust (PEB), which saw a steeper fall of 25.2% over six months and dwindled 34.3% over the past 52 weeks.

As a result, analysts remain moderately optimistic about its prospects. The stock has a consensus rating of “Moderate Buy” from the 17 analysts covering it, and the mean price target of $19.30 suggests a modest 35.8% premium to its current levels.

On the date of publication, Kritika Sarmah did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.